Helium is favored for cryogenic applications and temperatures close to absolute zero due to its chemical inertness. IDTechEx's report, "Helium for Semiconductors and Beyond 2025-2035: Market, Trends, and Forecasts" explores some of the main applications for helium, including supply challenges that threaten the helium market, with geopolitical risks surrounding its sourcing.

Being a finite resource, helium has been labelled a critical mineral in the EU and Canada, and semiconductor fabs manufacturing advanced chips for AI heavily rely on this commodity. Although supply is currently stable, it is a market that is known for its chronic volatility. IDTechEx reports that since 2005, there have been 4 known helium shortages that have all affected the availability and costs of the gas. As a result, new helium exploration efforts are emerging.

Helium's role in advancing semiconductor manufacturing

With the growth of AI workloads, there is a commensurate requirement for high performance chips such as GPUs and TPUs, which in turn rely on cutting-edge fabrication technologies.

According to IDTechEx's forecasts, semiconductor manufacturing in particular will be one of the main drivers for helium demand, as the complex and intricate production processes rely on the gas's thermal conductivity, chemical inertness, and high diffusivity. For example, helium is used as a coolant for advanced EUV lithography systems and also as a carrier gas in etching and chemical vapor deposition processes. In factory operations, it can assist with leak and safety testing, as well as creating an inert atmosphere. With the US Chips Act, EU Chips Act, and several other government initiatives worldwide to boost the semiconductor industry, IDTechEx's report "Helium for Semiconductors and Beyond 2025-2035: Market, Trends, and Forecasts" provides 10-year forecasts for helium demand for semiconductor and fibre optic manufacturing, and several other sectors.

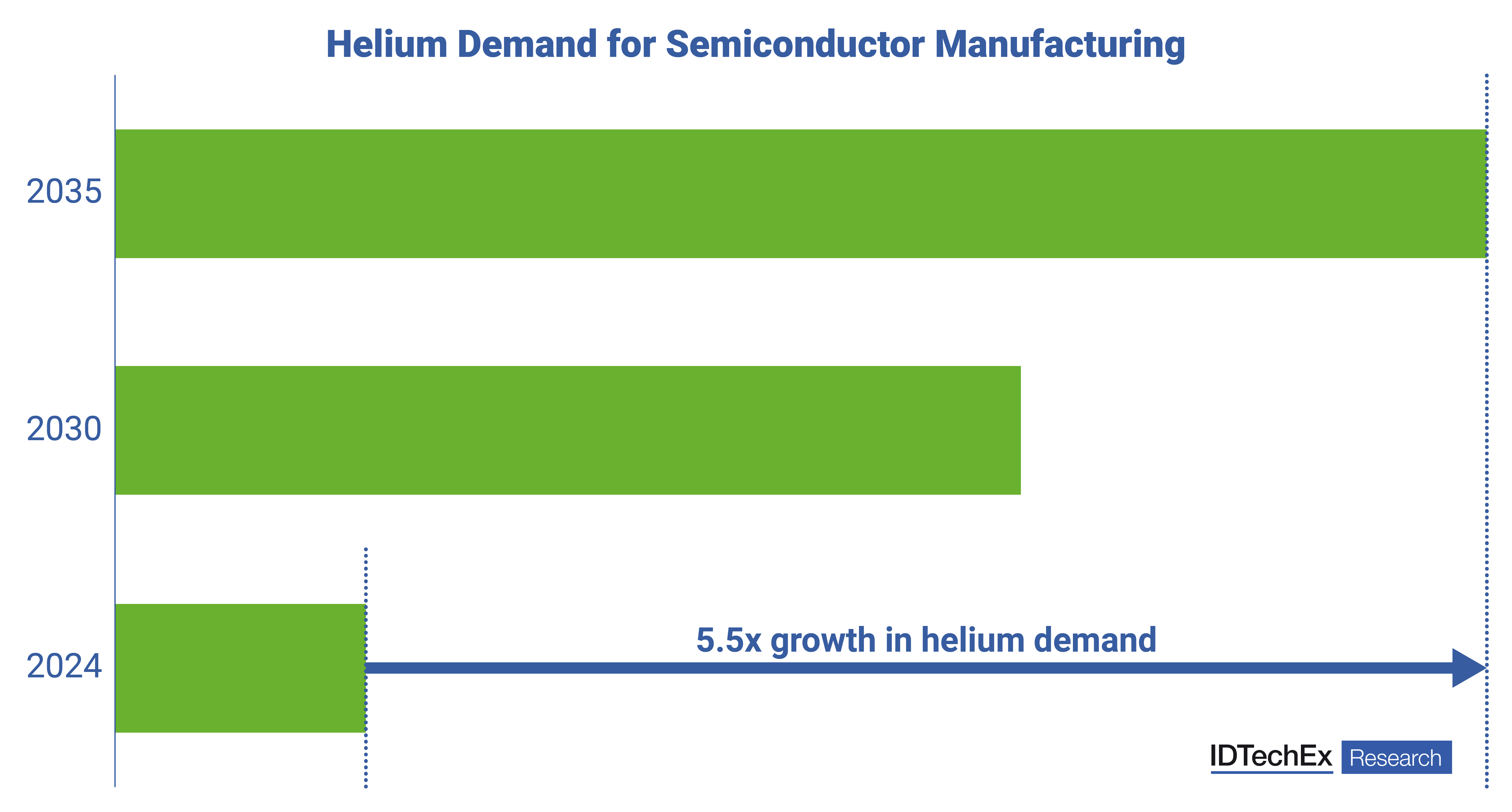

IDTechEx forecasts over 5-fold growth in helium demand for semiconductor manufacturing over the next 10 years. Source: IDTechEx.

Helium hotspots and developments

Most commercial helium is sourced as a by-product of natural gas where helium is present at very low concentrations. For these centralized gas processing facilities, helium recovery is generally integrated into cryogen nitrogen rejection units, which are only feasible when operating at a very large scale. These are typically followed by pressure swing adsorption (PSA) separation for further purification. Although helium production capacity is anticipated to increase with Qatar and Russia expected to ramp up production, it does not necessarily guarantee a disruption-free helium supply moving forward when considering geopolitical tensions in regions where helium is largely produced.

Within the US and Canada, there are growing opportunities for small players within the helium industry to access new hotspots within non-hydrocarbon gases in geological reserves, where concentrations of helium can fall somewhere between 0.3 and 10%. IDTechEx reports that low-capex separation systems, such as membrane and PSA technologies, can be used to upgrade and purify the helium acquired from these sources, with players adopting PSA, membrane, or a hybrid PSA + membrane system depending on the separation objective. IDTechEx's report provides comprehensive market analysis of these technologies, with product benchmarks and case studies.

For more information on helium separation technologies, supply, demand, and applications of helium, visit IDTechEx's latest report, "Helium for Semiconductors and Beyond 2025-2035: Market, Trends, and Forecasts", and the wider portfolio of Advanced Materials & Critical Minerals Research Reports and Subscriptions. More information on gas separation membranes can also be found in IDTechEx's dedicated report, "Gas Separation Membranes 2026-2036: Materials, Markets, Players, and Forecasts".